B2B payments, or business-to-business payments, refer to financial transactions between companies. They are crucial for ensuring smooth operations, maintaining financial health, and fostering strong business relationships.

This guide explores traditional methods, like checks and wire transfers, alongside cutting-edge digital platforms. Navigating the complexities of B2B payment processing, it addresses challenges and offers best practices to streamline financial transactions.

ON THIS PAGE

How Do B2B Payments Work?

Here’s a quick overview of how B2B payments typically work.

Step 1: Invoice Generation

The first step typically begins when one business provides goods or services to another. Most cases involve generating an invoice to request payment for the rendered products or services.

Step 2: Invoice Sent to Buyer

The seller sends the invoice to the buyer. This invoice includes essential and detailed information such as the due date, payment amount, payment terms, and details of the products or services provided.

Step 3: Payment Approval

The buyer’s accounts payable department reviews the invoice to ensure accuracy and compliance with agreed-upon terms. They may also verify that the goods or services were delivered as expected.

Step 4: Payment Method Selection

Buyer chooses a payment method based on their preferences and any agreements in place. Payment methods can include traditional options like checks and wire transfers, as well as digital methods like ACH payments or transfers, virtual cards, and e-wallets.

Step 5: Payment Execution

Once the payment method is selected, the buyer initiates the payment. The right payment solution or process varies based on the chosen method:

Traditional Methods

The most common method for checks is the buyer writes a check and mails it to the seller, who then deposits it in their bank account. Wire transfers involve the buyer instructing their bank to send a specified amount to the seller’s bank account.

Digital Methods

Buyers typically initiate ACH transfers, virtual card payments, and e-wallet transactions online by entering the necessary payment information and facilitating electronic fund transfers.

Step 6: Payment Processing

The payment goes through the chosen payment processing system. It can happen almost instantly in digital methods, while traditional methods may take several days to clear.

Step 7: Payment Receipt

The seller’s accounts receivable department receives the payment and verifies that it matches the amount on the invoice.

Step 8: Reconciliation

Payment is reconciled with the original invoice, ensuring that the payment corresponds to the services or products provided. This stage addresses any discrepancies or overpayments.

Step 9: Record-Keeping

The buyer and seller both should maintain transaction records, including the invoice, payment confirmation, and any related communication.

Step 10: Payment Acknowledgment

The seller acknowledges the payment and marks the transactions complete.

It’s important to note that the specific process may vary based on the payment method, industry, and the terms agreed upon between the buyer and seller. In addition, B2B payments can also involve international transactions, which may introduce additional complexities related to currency conversion, cross-border regulations, and compliance.

Did you know?

As per GlobeNewswire, the B2B payments market is set to reach USD 1,618.15 Billion by 2028, with a forecasted CAGR of 10.20% (2022-2028).

How to Choose the Right B2B Payment Processing Solution?

When selecting a B2B payment processing solution, businesses should consider:

- Security: The chosen payment solution must prioritize ecommerce security to protect your sensitive financial information and transactions.

- Integration: Ensure the solution seamlessly integrates with your existing systems to streamline your payment processes.

- Costs: Evaluate the upfront and ongoing costs associated with the payment solution to make an informed decision.

- Scalability: Ensure that the solution can grow with your business.

- Customer Support: Access to responsive customer support is vital in case issues arise.

- Digital Payment Platforms: As mentioned earlier, digital payment platforms like ACH transfers, virtual cards, and e-wallets are excellent choices for their efficiency, security, and cost-effectiveness.

- Online Portals for Purchase Orders: Businesses seeking to optimize their procurement processes find essential online portals that facilitate the creation and management of purchase orders.

Recommended Read: B2B Ecommerce Features

How can Businesses Streamline Their B2B Payment Transactions?

Businesses can streamline their B2B payment transactions by adopting some strategies and practices that enhance efficiency, reduce costs, and improve the overall process. Here are some key steps to achieve this:

Implement Digital Payment Solutions

Use modern, digital payment platforms or methods such as ACH transfers, virtual cards, and e-wallets. These solutions offer faster processing, reduced administrative overhead, and greater convenience.

Automate Payment Processes

Leverage automation to handle repetitive tasks like invoice generation, payment scheduling, and reconciliation. Automation reduces the risk of errors, speeds up processing times, and frees up human resources for more strategic tasks.

Read Next-Step-by-Step Guide On B2B Ecommerce Customer Journey

Centralize Payment Processing

Streamline B2B payment operations by centralizing payment processing functions. This reduces redundancy and makes it easier to monitor and manage payments.

Recommended Read: Takeaways: US B2B Buyers’ Online Purchasing Habits 2026

Optimize Cash Flow Management

Maintain a close eye on cash flow by using financial software that provides real-time insights into your company’s financial health. It helps you make informed decisions and avoid financial pitfalls.

Enhance Security Measures

Implement robust security measures to protect sensitive financial data. Multi-factor authentication, encryption, and regular security audits are essential for safeguarding against fraud and data breaches.

Establish Clear Payment Terms

Create transparent payment terms and agreements that clearly outline payment schedules and expectations. It reduces the risk of disputes and helps maintain healthy business relationships.

Regularly Monitor and Analyze Payment Performance

Continuously track payment data and analyze trends to identify areas for improvement. This practice helps you forecast cash flow, anticipate financial challenges, and make data-driven decisions.

Embrace Blockchain Technology

Consider the potential advantages of blockchain technology in B2B payments. Blockchain offers enhanced security, transparency, and smart contract capabilities, which can automate and secure payment processes.

Choose the Right Payment Processing Provider

Select a payment processing provider that aligns with your business needs and goals. Evaluate factors like security, integration capabilities, scalability, and customer support.

Streamline Cross-Border Payments

If your business engages in international transactions, use international payment services and currency conversion platforms to simplify the process. Staying informed about international regulations and compliance requirements is crucial.

Reduce Costs

Look for ways to reduce operational costs associated with payment processing. It could include consolidating banking relationships, negotiating lower fees, and automating cost management processes.

Regularly Update Payment Processes

Keep yourself informed about industry developments and regulatory changes. Continuously update your payment processes to remain competitive and compliant.

Recommended Read: B2B Ecommerce Statistics In 2026: Latest Updates & Trends

Popular B2B Payment Processing Providers

Choosing the right provider is a crucial decision. Here are some reputable B2B payment processing providers:

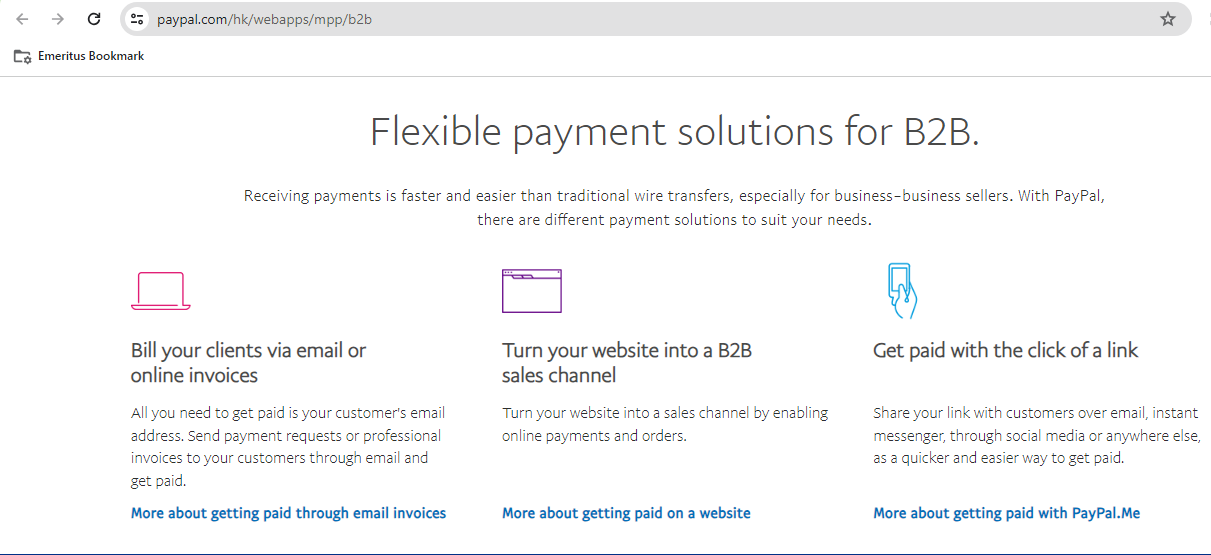

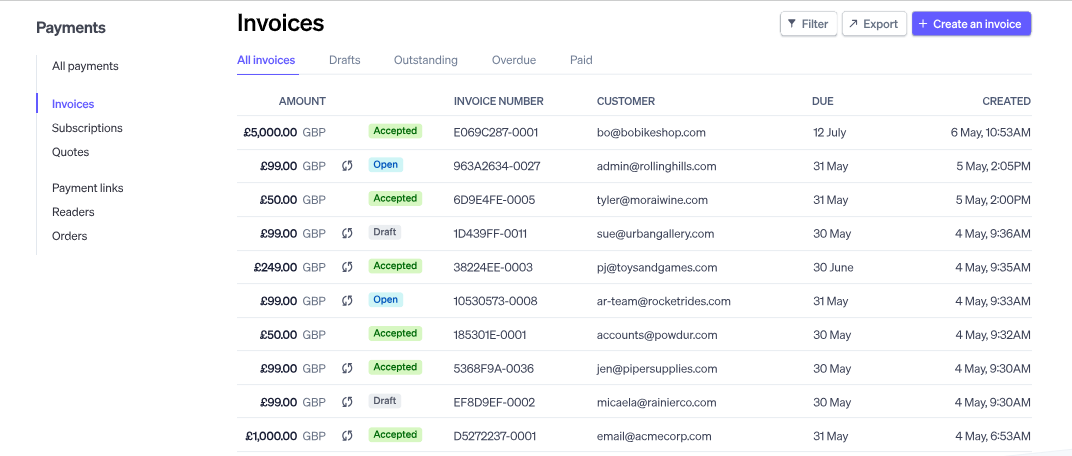

PayPal

Known for its flexibility and global reach, PayPal is a reliable choice for businesses of all sizes.

Stripe

A favorite for ecommerce businesses, Stripe offers comprehensive payment solutions.

Square

With its user-friendly interface and integrated hardware, Square is an excellent choice for small businesses.

Adyen

A global payment company, Adyen specializes in cross-border transactions and international expansion.

Braintree

Owned by PayPal, Braintree offers a simple integration process and support for different payment methods.

What Security Measures Should Businesses Consider for Secure Payment Processing?

Ensuring payment processing security is paramount for businesses in the digital age. The consequences of a security breach can be devastating, including financial losses, reputational damage, and legal repercussions.

Implementing robust security measures is crucial for safeguarding sensitive financial data and maintaining the trust of customers and partners. Businesses should consider the following security measures for secure payment processing:

- Multi-factor authentication: Requires users to provide multiple forms of verification for access.

- Encryption: Ensure data is encrypted in transit and at rest to protect against unauthorized access.

- Secure payment gateways: Use trusted and secure payment processing services to safeguard transactions.

- Regular security audits: Regularly assess to identify vulnerabilities and promptly address them.

- Employee training: Train staff to recognize and respond to security threats such as phishing attacks and fraudulent invoices.

- Strong password policies: Enforce complex password requirements to prevent unauthorized access.

- Firewalls and intrusion detection systems: Implement them to monitor and block suspicious network activity.

- Data access controls: Restrict access to sensitive financial information to authorized personnel only.

What are the Different Types of Transactions B2B Payment Methods Commonly Used?

Traditional Methods

According to research conducted by PYMNTS, 81% of businesses still use paper checks for B2B payments.

Paper Checks

Checks have long been a staple in B2B transactions. They offer familiarity but come with drawbacks like delayed processing, high costs, and manual handling, making them less efficient in today’s fast-paced business world.

Wire Transfers

The most common way wire transfers are known for their speed but can be costly and may require significant effort in terms of documentation and compliance.

Digital Payments

Automated Clearing House (ACH) Transfers

ACH transactions or transfers are electronic funds transfers that are becoming increasingly popular. They offer efficiency, lower costs, and quick processing, making them an attractive business option.

Virtual Cards

Virtual cards are one-time-use credit card numbers, providing enhanced security and control over payments. They are gaining popularity for their ability to reduce fraud and simplify reconciliation.

E-Wallets

E-wallets like PayPal and digital currencies like Bitcoin offer alternative ways to make and receive payments. They can be useful for businesses with international operations.

Read Also: The Ultimate Guide to B2B Wholesale Marketplace

The Emergence of Blockchain in B2B Payments

Blockchain technology, primarily associated with cryptocurrencies like Bitcoin, has the potential to revolutionize B2B payment processing. It offers enhanced security, transparency, and the ability to facilitate smart contracts, automating payment processes.

The Advantages of Adopting Secure Payment Processing Solutions

Implementing secure payment processing solutions brings numerous advantages to businesses:

Efficiency

Streamlined payment processes lead to faster transactions and reduced administrative overhead. Adopting digital payments and online portals offers a good choice for businesses aiming to expedite transactions.

Reduced Errors

Automation minimizes human errors, ensuring accurate financial records and a secure environment.

Cash Flow Management

Better visibility into cash flow enables more informed financial decisions.

Security

Protects against risk of fraud and data breaches, safeguarding sensitive financial information.

Global Reach

Enables businesses to engage in international business payment systems and transactions seamlessly.

What are the Challenges in B2B Payment Processing?

B2B payment processing, while crucial for the functioning of businesses, presents its fair share of challenges.

Security and Fraud Prevention

One of the primary concerns in B2B payment processing is security. Here are some of the challenges related to security and fraud prevention:

Challenge 1.1: Payment Fraud

Payment fraud comes in various forms, such as identity theft, unauthorized access to financial data, and fraudulent invoices. Businesses are at risk of making payments to the wrong recipients, falling victim to impersonation, or processing fake invoices.

Challenge 1.2: Data Breaches

Data breaches can expose sensitive financial information, jeopardizing the financial health of both parties involved in the transaction.

International Payments

Cross-border transactions are commonplace in the B2B industry. However, international payments come with their own set of challenges.

Challenge 2.1: Currency Exchange

When businesses deal with international transactions, they often face currency exchange challenges. Fluctuating exchange rates can affect the value of transactions, leading to financial losses or gains.

Challenge 2.2: Regulatory Compliance

Different countries have varying regulations governing international payments. Navigating these regulations can be complex and time-consuming.

Challenge 2.3: Hidden Fees

International payments are often associated with hidden fees, including intermediary bank charges, currency conversion fees, and foreign transaction fees.

Improving Efficiency and Reducing Operational Costs

Efficiency and cost-effectiveness are critical in B2B payment processing. Inefficiencies can lead to delays, increased costs, and strained relationships with vendors and partners.

Challenge 3.1: Manual Processes

Many businesses still use manual processes for tasks like invoice generation, data entry, and reconciliation, which can be time-consuming and error-prone.

Challenge 3.2: Multiple Banking Relationships

Dealing with numerous banks and financial institutions can increase costs and complexities in managing B2B payments.

Challenge 3.3: Late Payments

Late payments can disrupt cash flow and strain relationships between businesses. Inefficiencies in payment processes often lead to delayed transactions.

Optimizing B2B Payment Solutions for Long-Term Success

Whether opting for traditional cash payments or embracing cutting-edge electronic payments, businesses catering to a diverse consumer base can make informed choices. From the most common methods to American Express and various digital payment options, understanding and utilizing diverse payment solutions is crucial.

B2B payment processing is a critical component of any business’s financial operations, and by implementing best practices, staying informed about the latest developments, and addressing security concerns, your business can thrive in the modern economy.

FAQ

What is B2B payment processing?

B2B payment processing refers to the complex web of financial transactions between businesses. It encompasses things like sending and receiving payments, managing invoices, and reconciling accounts. In essence, it’s the backbone of the financial ecosystem that allows businesses to operate smoothly.

Why do many businesses prefer using electronic transfers over traditional payment methods?

Electronic transfers are faster, more efficient, and cost-effective compared to traditional methods like electronic checks and wire transfers, making them a popular choice among businesses.

How do B2B payment processors facilitate transactions, and what are their benefits?

Most popular B2B payment processors offer secure and efficient payment processing, simplifying transactions and reducing the risk of errors and fraud.

What is the main difference between B2B and B2C payments?

The main difference between B2B (business-to-business) and B2C (business-to-consumer) payments lies in the transactions. B2B payments involve businesses conducting financial transactions with other businesses, while B2C payments involve businesses selling products or services to individual consumers.

What are the most common B2B payment trends in recent years?

Some common B2B payment trends in recent years include the increased use of credit cards, the adoption of digital payment methods, and the growth of the ecommerce industry. These trends reflect a shift towards more convenient and efficient payment methods.

What are the advantages of using B2B payment solutions for high-value transactions?

B2B payment solutions are advantageous for high-value transactions and high processing costs due to their efficiency, security, and ease of use. They offer a seamless way to handle large payments, reducing the risk of errors and delays.

What is the role of credit card associations in B2B payments?

Credit card associations play a significant role in facilitating B2B payments by providing the infrastructure and networks for credit card processing. They ensure that businesses can accept credit card payments from their clients, enhancing the ease of doing business.

How do B2B payment trends affect small business owners and merchants?

Staying updated with B2B payment trends is essential for business owners and merchants to remain competitive and take advantage of evolving payment solutions that can enhance their operations.

How do debit cards fit into B2B payment processing?

Debit cards can be used for B2B payments, offering a convenient and widely accepted payment method. They are useful for smaller transactions and everyday expenses in business operations.